This website uses cookies to help improve your user experience

When a company decides on a new payment gateway integration, the reasons behind it are typically driven by very specific business needs.

Whether it’s about enabling customers to use a new payment method popular in their region or fixing long-lasting issues with existing ones, this effort is meant to maximize the number of successful payments, reduce the cost per transaction, and drive up user satisfaction and revenue.

Since the majority of payment solutions come bundled with robust APIs and detailed documentation, fintech payment integrations are often viewed by tech leaders and business stakeholders as a fairly straightforward undertaking.

The truth is, they aren’t.

We’ll explore real-world scenarios with Andrey Karazey, Oxagile’s Senior PHP and Python Engineer, who shares his hands-on experience with payment integrations in fintech projects.

Key takeaways:

In reality, the scope of payment integration development projects spans far beyond plugging the right API calls into existing code. It requires a multitude of technical infrastructure decisions, compliance with data security frameworks, and close attention to essential user experience nuances.

On top of that, practice shows that very few payment integration projects follow an optimistic trajectory. Edge cases are surprisingly common and solutions often imply far more than just code edits, occasionally leading to operational changes to accommodate payment requirements.

The complexity of the process becomes even more apparent if we factor in the potential challenges associated with having several payment systems working in an ensemble.

Let’s take a look at the most important practical aspects of payment integrations, as well as the important long-term business impact of building scalable payment solutions from the get-go.

Not every payment gateway out there works the same way. The implementation approach in each case depends on how much control you want to have over the checkout experience, your readiness to take on the often hefty compliance overhead, and the geos you intend to serve.

With a hosted gateway, the user leaves your site temporarily to complete the transaction on the payment processor’s secure page. A good example would be PayPal or Stripe. Because your customers’ card data never lands on your servers, your PCI DSS scope shrinks dramatically, which is always a positive thing. The tradeoff, however, is less control over the UX and an extra redirect that may increase the drop-off rate in certain conditions.

In this scenario, payment information fields are placed on your own pages, giving you full and undivided control over the look and feel. The caveat is that you’re now a part of the payment data flow, which means stricter PCI requirements and more responsibility. This model is more common in enterprise environments where brand style consistency and higher conversion can justify the extra security overhead.

This is the most flexible model where payments are handled entirely through API calls to the payment gateway provider with no external redirects and no prebuilt interfaces. It’s a common choice among fintech platforms, popular marketplaces, and subscription-based businesses that need payment logic embedded deeply into multiple application workflows. This scenario is technically the most complex but offers the deepest level of integration.

Such payment gateway types are usually region-specific and support local payment systems. In addition to allowing you to use local payment methods, they often offer better approval rates, lower interchange, and feature user interfaces adapted to the expectations of local consumers. These kinds of gateways are essential for any business with serious international ambitions.

As is often the case, the final implementation model is rarely just one or the other. Many companies opt for hybrid options that combine a primary API gateway with local providers or even have a hosted fallback route for some flows.

Payment integrations are never just a technical feature. In high-volume online businesses, payments are inseparable from operations, finance, and customer relations in terms of importance. So treating them as “just another integration” may turn out to be a costly mistake later down the road.

And since we view payments as part of the core business infrastructure where a small bug can translate into massive losses, it is vital to build upon architectures that deliver scalability, resilience, secure payment processing, and performance at the same time.

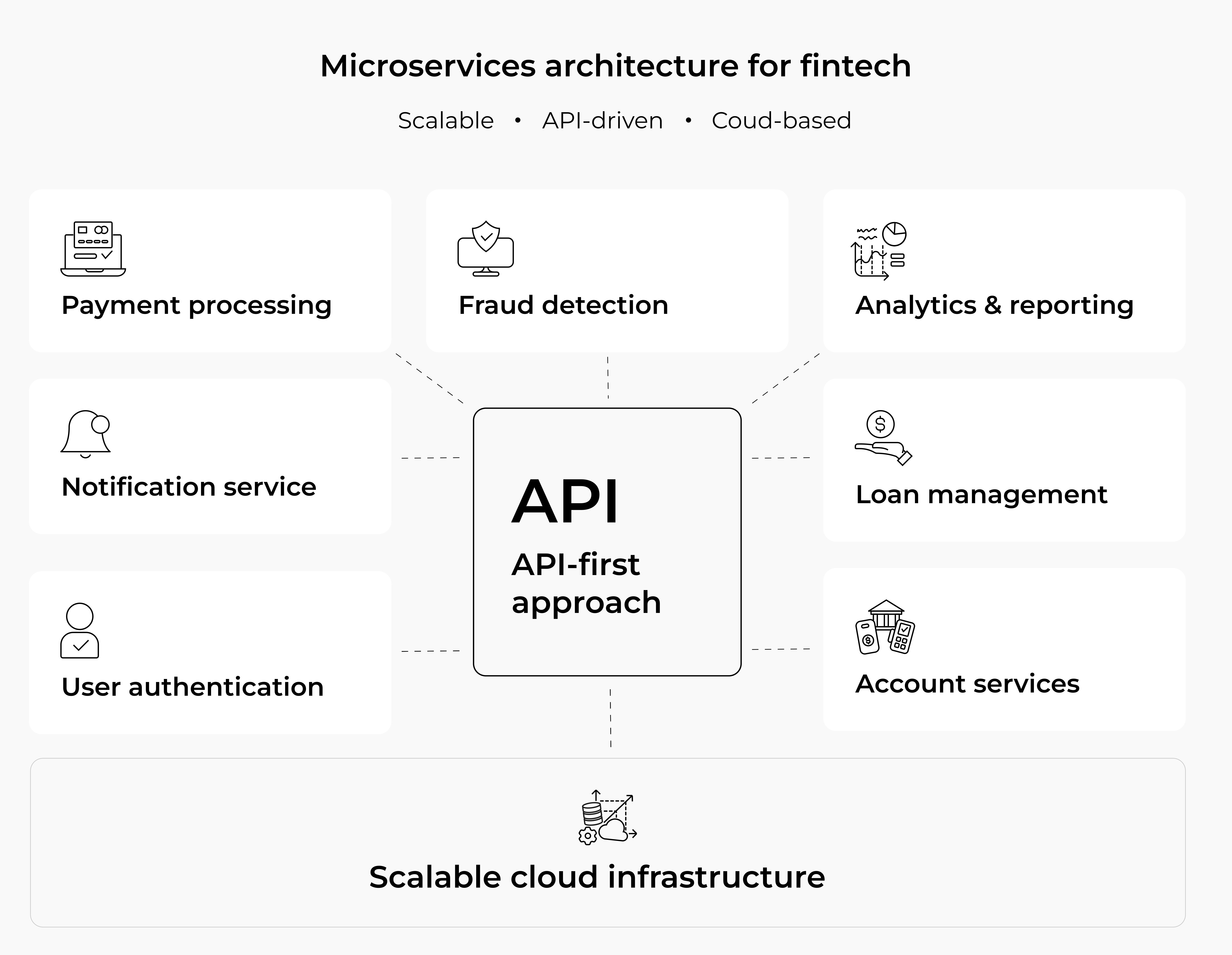

Today’s payment architectures are predominantly based on microservices where each component is responsible for a particular function, such as payment authorization, reconciliation, routing, fraud detection, or compliance monitoring. This modularity provides distinct advantages over traditional monolithic systems:

Building with microservices is one way of addressing potential scalability and stability challenges, but there is one more extremely important architectural approach that will prime you for anything coming your way in the future.

Today, every multi-payment method integration should ideally be built around APIs (Application Programming Interfaces). This approach creates a stable, abstract, unified interface, which allows you to continuously modify and improve your system without worrying about downstream apps and services.

On the other hand, it dramatically facilitates interactions with third-party payment service providers (PSPs) and payment orchestration platforms like Adyen, Primer, Braintree, or Stripe.

A combination of a flexible, decentralized architecture based on event-driven, cloud-native microservices with a robust API interface is the most surefire way of making your system future-proof and easy to modify.

The rule of thumb here would be to design fintech payment integrations as infrastructure elements as opposed to a one-time, rigid connection to a PSP. A solid payment architecture assumes that the next provider change will inevitably happen and you’ve got to have everything in place to make the switch as painless and quick as possible.

How do you pave the way to faster payment service provider integrations, centralized control over the entire infrastructure, and dramatic growth of payment acceptance rates in key regions?

This case demonstrates how an API-centric approach and experience in developing cloud-native apps helped Oxagile build a custom integration layer for a client that reduced new PSP integration time by 80%, improved security and performance across the board, and boosted payment approval by a whopping 30%.

Data format issues may not seem like a serious concern initially, but in real-life scenarios, they rank high up on the list of things consistently leading to payment failures.

Each time a transaction is posted with even a single data formatting issue, the receiving end is likely to reject it right off the bat — even before passing it to the bank for authorization.

The most common standard regulating debit and credit card transactions is ISO 8583 with its 128 supported fields. Authorizing banks rely on complex logic that analyzes different combinations of these fields to make an authorization decision.

These core parameters are often augmented with additional data captured at the pre-authorization stages by vendors and networks like Visa and Mastercard and then processed to fit into standard ISO 8583 fields.

An efficient solution to lowering declines due to data issues is to focus on building effective validation mechanisms based on the ISO 8583 standard and payment providers’ proprietary guidelines. At the very minimum, they should cover the following:

Companies that observe high data quality standards will always have the edge. Lower payment decline rates translate directly into fewer customer support escalations and consistent field completion leads to lower transaction fees.

The difference between a decline and an approval is often small. Learn how we help businesses close that gap.

Routing is undeniably one of the most essential components of modern fintech payment integrations. By definition, routing is the process of switching between payment methods depending on the context and immediate needs. The purpose of routing is to provide the best user experience while minimizing transaction costs and payment declines for the vendor.

Routing comes in two main flavors: static and dynamic. Static routing relies on predefined rules: for example, choose gateway X for domestic payments and gateway Y for international cards. However, this approach has limited cost- and performance effects due to its inflexible nature. This limitation is what makes smart, dynamic routing necessary.

Unlike static routing, dynamic routing instantly (typically within milliseconds) analyzes each transaction and identifies the optimal processing scenario based on a variety of factors, including:

The routing logic is defined by transaction metadata, user behavior, purchase history, and other relevant parameters.

Expert opinion:

“A single PSP works until it doesn’t, and when it breaks, everything breaks at once and your hands are tied. Orchestration turns payments from a single point of failure into a system you can actively optimize for cost, reliability, and growth.”

Routing is not just a forward-facing process. It has a useful flip side as well. When a payment is declined by a PSP for some reason, a properly implemented intelligent fallback logic instantly selects the next most suitable payment gateway to process the transaction. The routing algorithm can use various triggers and conditions.

With an orchestrated fallback mechanism in place, instead of puzzling the customer with a single “payment declined” message and turning them away, the system retries through a cascade of alternative providers, recovering transactions that would otherwise fail.

According to Primer1, merchants using intelligent fallback strategies achieve payment recovery rates up to 20%, which is a sizable chunk of revenue that would otherwise be lost.

In the context of payment gateway integration, UX extends far beyond sleek UIs and on-screen ergonomics. Bad user experience directly translates into lower conversions and lost revenue. And when it’s combined with data format inconsistencies, complexity of the authorization or payment flows, as well as other issues across the board, it may substantially affect your business performance.

The key principles of good UX for payments can be broadly summarized by the following points:

This case from our team focuses not just on a seamless, end-to-end migration of a massive, live customer base to an alternative PSP, but also on implementing a smooth, frictionless 3DS authentication process and building a custom payment gateway for notable performance gains and cost optimization.

It would be impossible to discuss secure payment processing without mentioning security. This is a fundamental element of each and every system that handles sensitive data and operates in multiple jurisdictions. This domain is regulated by a number of standards, including ISO 27001, PSD2, SOC 2, and, most importantly, PCI DSS.

The majority of modern fintech payment integrations do not aim to fully meet PCI DSS requirements on their own — that is a very serious and expensive legal, technical, and procedural challenge that bears a lot of risks and responsibilities. Instead, they rely on payment service providers and payment platforms that are already PCI DSS compliant.

The common practice in the industry is to never store raw card data and use card data tokenization wherever possible, combining it with hosted fields and smart redirect flows to reduce your own PCI DSS scope to the greatest extent possible. On top of that, 24/7 payment monitoring and incident response management are must-haves for any modern business relying on an uninterrupted flow of payments.

The golden rule in the security department is “the less you store, the less likely you are to be responsible for when something goes wrong” — and this rule is not to be underestimated.

Expert opinion:

“The easiest compliance program is the one you never have to run. When payments are designed so sensitive data never resides in your systems, compliance becomes an architectural property, not an ongoing struggle or source of concerns.”

The payment gateway integration process consists of several stages that combine operational planning, compliance checks, and payment software development activities.

When designed with scalability, functional separation, and modularity in mind, this process allows businesses to add or replace payment providers without massive reengineering efforts.

The actual cost of payment gateway integration varies extremely broadly and generally lies between $10,000 for the simplest single-provider integration and $100,000+ for building an entire payment infrastructure with complex routing and orchestration, let alone AAA projects also involving payment gateway migration.

Several factors typically influence the final cost:

Because of all these and other variables, the cost of payment integration projects falls within a very broad range: from a relatively modest engineering effort for a single provider to ultra-complex infrastructure projects for large fintech platforms. The cost of each project can only be estimated after thorough analysis and consideration of all relevant factors.

Quality payment integrations are challenging and rely on a great deal of multidisciplinary expertise. From future-proof, decentralized architectures with API-first genes to advanced security features and intelligent payment routing — all of these components need a holistic understanding of the fintech scene and its constantly evolving cross-border requirements.

The success of each multi-payment method integration project relies heavily on your or your vendor’s ability to see the road ahead, build complex payment orchestration layers with sophisticated routing and failover logic, and a confident grasp of global and regional data security regulations.

In the end, companies that treat payment integrations as long-term infrastructure initiatives and not one-off projects come on top. Payments demand ownership, not handoffs, and this should be the primary guiding principle for any business venturing into this territory.

We help teams move beyond quick fixes and build payment systems meant to last.

1. Merchants using Primer’s Fallbacks solution have seen a recovery rate of up to 20% – Primer

2. Almost 50% of payments are made by guest shoppers – PayPal

3. Single payment method statistics based on a major study from Ecommpay and IMRG – FinTech Magazine

Secure payment processing reduces the risk of breaches and fines while preserving user trust, which directly protects revenue and long-term brand value.

Scalable payment solutions can absorb higher volumes, new providers, and new regions without major rewrites, so growth plans are not bound by technical limitations.

Multi-payment method integration aligns checkout with how different user groups actually prefer to pay, which increases conversion, supports regional expansion, and reduces dependence on any single payment provider.

When security controls are embedded into your core architecture, every new provider or method can reuse the same safeguards and evidence, making due diligence and audits faster and less burdensome.

They should look for the ability to add or replace providers quickly, keep decline and error rates stable as volume grows, and support new markets without revamping core systems.

A solid payment gateway provider should offer strong security, a wide selection of payment methods, clear and transparent fees, as well as well-documented APIs for smooth integration and future scaling.

A scalable payment solution can handle growing (and spiking) transaction volumes, have the flexibility to support new markets and payment methods, and be able to integrate additional providers without major architectural rework.