This website uses cookies to help improve your user experience

If you are browsing the market for a payment service provider (PSP) for your current or upcoming project, you may soon discover that most of the options look surprisingly similar.

The majority of payment services support the same payment methods, have fairly comparable commissions, and come with highly functional, convenient APIs. But the day integration begins, important differences may start kicking in:

This is exactly the reason why many teams don’t really struggle with the choice of a payment service provider, as there are plenty of perfectly good ones out there. Instead, they often have a hard time dealing with what happens after the service is paid for and when the work is well underway.

In this article, we’ll walk through a list of online payment service providers and look beyond raw features, examining how these platforms actually behave in production. We’ll also share practical insights from our own experience with payment integrations to demonstrate where complexity typically hides and what teams often severely underestimate when choosing a provider.

Key takeaways:

A payment service provider is what allows your website or online store to actually accept payments from customers by securely connecting your checkout flow to card networks, banks, and alternative payment methods.

PSPs are integrated, all-in-one solutions. Instead of bridging together several third-party components, a PSP conveniently bundles everything into one:

So instead of having to deal with three integrations, you only need to get one right. At least that’s the promise you see on their landing pages. Also, integrating a commercial product into your website is a substantially lower investment compared with the payment gateway cost if one is built from scratch.

In practice, however, the bulk of integration complexity does not revolve around core features — they typically work as expected. It sits on the perimeter and in not-so-obvious edge cases that teams can’t always fully foresee while putting together an initial payment service providers list.

This complexity shows up in the parts no one really thinks about right away: for example, how refunds behave across different payment methods, or what happens when a payment is authorized but never gets captured, or how reliably transaction details make their way into your internal systems.

To give you some perspective, our payment software development experience is full of PSP examples where a refund was successfully processed on the PSP side, but never reflected correctly in the company’s reporting, creating reconciliation gaps at month-end. Or situations where a payment flow worked perfectly with debit/credit cards, but fell apart when a local payment method used asynchronous confirmation.

With that in mind, the real differences between PSPs become clearer when you look beyond the declared functionality and see how they behave in real integrations.

In one of our projects, we helped a company evolve from a single PSP setup to a multi-provider architecture to improve reliability and reduce regional transaction failures.

Instead of a simple switch, this required building an integration layer. And it all happened in a running live production environment without disrupting active transactions.

A company looking for the perfect PSP on the market would have zero problems finding one. Options range from globally recognized platforms to highly specialized, yet lesser-known regional payment solution service providers.

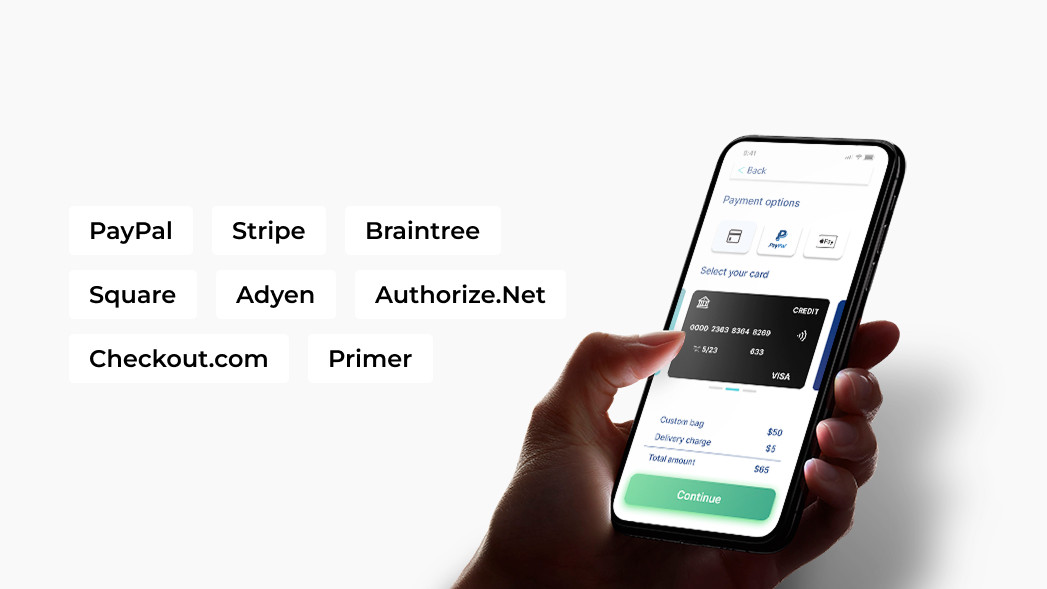

To give you some payment service provider examples, we put together a list of the most popular options available today. This is not a feature comparison table, but rather a reflection of how they tend to behave once real transactions start going through.

The go-to for developer teams who want full control and are comfortable handling the associated backend complexity. More than 195 countries, 135 currencies, and 100 payment methods, and various pricing tiers.

Not the cleanest integration, but customers recognize it and often expect to see it at checkout. Quick setup makes it a practical choice, though fees can vary depending on payment type and region.

A practical option for subscription businesses that need recurring billing, card vaulting, and PayPal support under one integration. Offers flexible pricing with standard per-transaction fees and no monthly charges.

Works well if your business operates both online and in person and you want one system for both. Has straightforward flat-rate pricing that’s easy to predict.

Built for enterprise scale. Comes with a commensurate level of implementation complexity. Pricing is tailored and depends on region, volume, and payment methods.

Dated developer experience, but stable and widely adopted. Still a solid choice if you don’t need a cutting-edge API, with predictable pricing that includes a monthly gateway fee plus per-transaction charges.

Good fit for teams that want more visibility and control over how payments behave, not just whether they go through. Offers flexible pricing tailored to volume, regions, and payment methods.

Sits on top of your PSPs instead of replacing them, which is useful when you need to route across multiple providers or want redundancy built in. Pricing on demand, but typically based on usage and setup complexity.

Let our experts walk you through this long payment service providers list and pick one that will work perfectly for your project and save you time and money during integration.

With years in the industry, we know exactly what determines how well payments work over time, what architectural decisions should be made, and how the entire system should be configured to make sure your revenue flow does not dry up at any point.

The PSPs above represent some of the most value-packed options available today, each with a distinct set of strengths and a slightly different integration approach. But knowing what each one offers doesn’t automatically tell you which one belongs in your stack.

When combing through a vast pool of payment services examples, feature-by-feature comparisons will only get you so far.

At a certain point, most providers can handle transactions. What actually matters is how they behave once payments start flowing through real scenarios and how much extra work they create around them.

A few pre-flight checklists will help separate a good fit from a costly one.

This is worth testing early, not after launch. Look at:

The key question is whether payment states remain clear and predictable at every step. If statuses feel unclear or hard to trace, be prepared to implement additional backend logic just to keep things in check.

Payments don’t just end at checkout. They still need to make sense in reporting. Check:

If reconciliation relies on spreadsheets or manual fixes, the integration is likely to become a massive ongoing operational burden (and a pain in the neck).

A PSP may perform well in one region and fail to meet expectations in another. Pay attention to:

Inconsistent behavior across geos often requires extra normalization logic on the backend.

Some setups are easy to integrate but difficult to change in the future. Look for:

The more tightly coupled the out-of-the-box setup is, the more expensive future modifications become.

Even if a single PSP is enough today, this may not be the case later down the road. To avoid PSP lock-in, you may want to explore the advantages of having multiple payment gateways in the future. Consider:

If adding a second PSP requires re-architecting the system, that cost is simply deferred and not avoided.

What most PSP comparisons don’t tell you: PSP decisions often lead to re-architecture later, especially when expanding to new regions or adding providers. What starts as a simple integration can evolve into orchestration, routing, and reconciliation challenges that require a completely different system design.

And there’s no “ultimate” payment service provider that fits every business. It’s always a set of trade-offs that either align with your setup or make you change it. Stripe, Adyen, PayPal, and others all solve the same core problem, but they do it in ways that shape your architecture, your operations, and your ability to evolve later.

The right choice is the one that checks the most boxes under your real conditions: your markets, payment flows, reporting needs, and plans for growth. Get that alignment right, and payments become something you don’t have to think about. Get it wrong, and it’s something you’ll be fixing long after launch.

Choosing a PSP is one of those decisions that looks simple at the start and gets expensive if done wrong. If you want to get it right from the beginning or fix an existing setup to stop leaking revenue, let our experts offer recommendations and practical help.

With a diverse project portfolio spanning over 20 years of software engineering, we have everything it takes to analyze your business case in detail and match it with the most efficient, scalable, and future-proof payment service provider in the market.

Tell us about your setup and we’ll tell you exactly where to go from here.

There’s no universally cheapest PSP. The implementation cost depends on your region, payment methods, and volume of transactions. Nominally lower fees can be offset by higher integration or operational overhead.

A payment gateway captures and securely transmits payment data, while a payment processor handles the actual transaction between banks. Most PSPs bundle both into a single solution.

Yes, reputable PSPs are natively PCI DSS-compliant and handle sensitive payment data securely. In practice, they also reduce your compliance burden by keeping card data off your systems.

Yes, and many businesses eventually do. A multi-PSP setup can improve reliability and flexibility, but it requires proper orchestration and adds architectural complexity.